The Impact of an Aging Population on the Med Device Space

I’m in the +65-age category and, if you’re like me, you are tired of hearing anecdotes. Here are some facts.

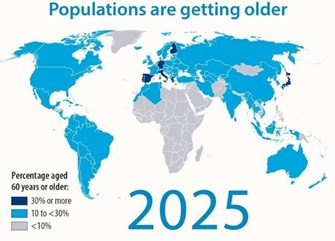

There are roughly 331,000,000 US residents today 1 and nearly 17% of those are 65 years of age or older. This segment of the population is expected to increase at an annualized rate of 3.1% over the next 5 years reaching 65.2 million in 2025 2. This compares to the annualized growth rate of the TOTAL US population of 0.7% during the same period! (Keep in mind, culture dies at a growth rate below 2.1%.)

Did you get those numbers? The +65 crowd will be growing at a pace of 4x the rest of the population.

Med Device Effects

A favorite mentor left me with one of my favorite euphemisms, “Never forget Randy, the first liar doesn’t stand a chance.” That sounds sarcastic but the “wonders” of the internet have made it increasingly difficult to separate the wheat from the chaff.

In a normal year, an aging population would be a boon for Device makers because there is a direct correlation between that age group and elective surgery. COVID has changed all of that for the near-term but the circle will be unbroken and we will see elective surgery rebound.

So, what has really changed? I’m going to try to stay apolitical and not get into how critical it has been to expose China for what it is. Notwithstanding, the impact to Supply Chain has been critical and taught business a lesson about their constant search for the cheap way out and how important closely held IP has always been.

The other impact that cannot be ignored is M&A or the adage that, apparently, bigger is better. The interesting side effect of M&A growth has been that as Device makers get bigger, their internal inertia grows exponentially and they find themselves unable to pursue R&D in a cost-efficient manner.

In the last 20 years, this has led to a plethora of exceptionally successful Device Start-Up companies who frequently find themselves selling X product to one of the major players and quickly moving on to XX product which is also acquired. While the large companies are acquiring technology rather than developing it, the reality may be that ‘necessity is the mother of invention’. (I know, Agatha Christie did NOT believe it to be true but per modern norms I’m adopting it to my purpose.)

Back to the data 3

In an estimated total market of $93.6B, Surgical Instruments should comprise 48.4% of the revenue, Surgical Appliances about 34.2%, Dental lab Equipment about 5.9%, and Dental Supplies about 5.6%. The shift has been that physician visits directly impact revenue in the segment and COVID had caused a dramatic reduction in these visits. Additionally, in the last 10 years, the number of hospitals acquiring local practices has risen dramatically as they combine GPO buying power with more control over purchasing in the Doctor’s office.

The market will continue to grow but I am not going to be the “first liar” and attempt to project the rate. The risk to US-based manufacturing will continue to be how much of that technology stays here versus getting shifted O-US as the numbers still seem to indicate an imbalance of domestic versus imported product over the next 5 years 2.

Summary

There are no real conclusions here. I hope that we have learned a lesson and that data will continue to help move us in the right direction. I am a HUGE supporter of US-based manufacturing; that’s where I started my career at the age of 18. I’m an equally big cheerleader for the Med Device world as I worked in it for 15 years and have recruited there for another 15. I suppose the lesson I see as most important is that we have to stop the pillaging of US developed IP in favor of a Global Economy.

My advice? Pay attention. You can’t use a search engine as a stand-alone source for the truth unless you’re only looking for the truth as told by that source. Dig, dig, and dig deeper, you’ll be as surprised as I was by what you find!

Footnotes:

- According to UN data

- From the IBISWorld Medical Instrument & Supply Manufacturing Report

- Excerpts from the IBISWorld report